Take-home grocery sales in Ireland increased by 5% in the four weeks to 23 January 2023, according to the latest data from Kantar, with grocery price inflation driving value sales growth rather than volume driving market growth. In January, average price per pack rose 14.6%, while volume per trip was down 13%, showing the challenges Irish shoppers are facing.

In the 12-week period to 23 January 2023, take-home grocery sales increased by 6.8%, with shoppers contributing an additional €211.8m to the overall market performance. As a result, shoppers spent an additional €90.50 per household year-on-year.

Emer Healy, Senior Retail Analyst comments: “The sector growth comes as grocery price inflation hit 16.3% - the highest level seen since Kantar started tracking grocery inflation. However, this does trail just behind Great Britain where inflation hit 16.7% after two months of slight decline. Irish households will now face an extra €1,159 on their annual shopping bills if they don’t change their behaviour to cut costs”.

Shoppers trade down after Christmas indulgence

Emer Healy, Senior Retail Analyst adds: “With consumers keeping a close eye on their purse strings after indulging during the festive period it’s no surprise that shoppers continued to trade down to supermarkets’ own label products this period, with sales rising 10.4%, well ahead of a 4.7% increase in branded lines”.

Sales of premium own label lines have reached €152.6m, up €5.7m from last year with €26.7m of that coming from premium own label chilled convenience products in the 12-week period, a strong growth of 11.6%. Value own label lines saw the strongest growth, up 34% year-on-year with shoppers spending €17.9m more on these ranges.

The Irish grocery market is more competitive than ever before, with shoppers looking for the best deals and retailers looking to retain customers. This is reflected by many supermarkets using their loyalty schemes to help shoppers save. According to Kantar’s LinkQ data, nearly 38% of shoppers claim to always use a money saving voucher. As a result, the amount bought on promotion has fallen to 27.7%, the lowest level for five years, exaggerating the usual post-Christmas drop off in deals.

However, government action to help consumers manage cost of living pressures may have bolstered shopper confidence as the number of households who classified their financial situation as struggling fell from 32% in October to 23% in December 2022, with just over half of Irish shoppers (52%) feeling they were managing financially.

Many Irish shoppers kicked off 2023 with good intentions, making health a priority. Shoppers spent an additional €848,000 on vitamins and mineral supplements. ‘Veganuary’ saw sales of meat-free alternatives grow 4%, with shoppers spending an additional €102,000 on tofu. ‘Dry January’ also saw sales of non-alcoholic beverages grow 4.6%, with 5% of Irish households purchasing a non-alcoholic beverage during January.

Irish retailer performance update

Online sales remained strong during January, up 5.6% year-on-year with shoppers spending an additional €8.5m in online channels. An influx of new shoppers boosted online sales, with nearly one in five Irish households now purchasing online.

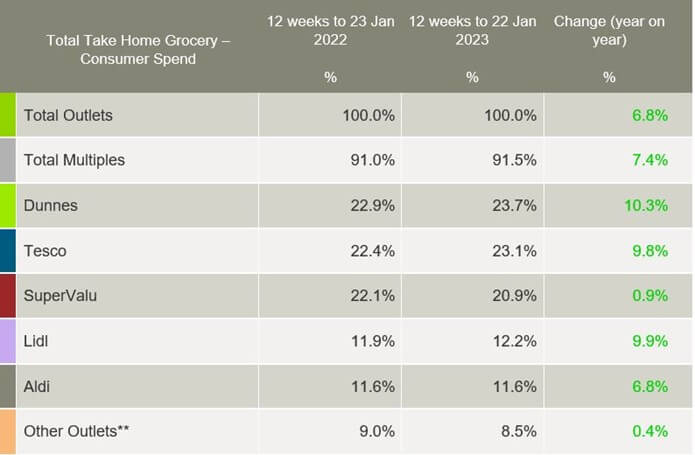

Dunnes Stores holds the highest share amongst all retailers at 23.7% with growth of 10.3% year-on-year. This growth stems from an influx of new shoppers in-store, up 1.34 percentage points, and shoppers returning more often contributed an additional €24.9m to their overall performance. Tesco is close behind with 23.1% market share and growth of 9.8% year-on-year. Tesco also has the strongest frequency growth amongst all retailers, up 10% year-on-year.

SuperValu holds 20.9% of the market and 0.9%. growth. Among the Irish grocery retailers, SuperValu shoppers make the most trips in-store with 20.8 trips on average, up 9.2% year-on-year. Lidl holds 12.2% share and 9.9% growth year-on-year. New shoppers and more frequent trips contributed an additional €25.5m to its overall performance. Aldi holds 11.6% and 6.8% growth year-on-year, with new shoppers and more frequent trips contributing an additional €10.8m to its overall performance.